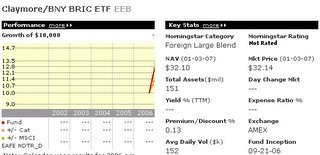

An Emerging Market ETF to Consider

posted by writing staff @ 1:32 PM

0 comments

![]()

![]()

A forum to share advice, ideas, and investment suggestions. Featuring Stocks and ETF's and Supporting Literature

posted by writing staff @ 12:55 PM

0 comments

![]()

![]()

posted by writing staff @ 12:11 PM

0 comments

![]()

![]()

posted by writing staff @ 12:05 PM

0 comments

![]()

![]()

How ETFs work?

by ETFZone staff

ETFs are securities certificates that state legal right of ownership over part of a basket of individual stock certificates. Several different kinds of financial firms are needed for ETFs to come into being, trade at prices that closely match their underlying assets, and unwind when investors no longer want them. Laying all the groundwork is the fund manager. This is the main backer behind any ETF, and they must submit a detailed plan for how the ETF will operate to be given permission by the SEC to proceed.

In theory all that a fund manager needs to do is establish clear procedures and describe precisely the composition of the ETF (which changes infrequently) to the other firms involved in ETF creation and redemption. In practice, however, only the very biggest institutional money management firms with experience in indexing tend to play this role, such as The Vanguard Group and Barclays Global Investors. They direct pension funds with enormous baskets of stocks in markets all over the world to loan stocks necessary for the creation process. They also create demand by lining up customers, either institutional or retail, to buy a newly introduced ETF.

The creation of an ETF officially begins with an authorized participant, also referred to as a market maker or specialist. Highly scrutinized for their integrity and operational competence, these middlemen assemble the appropriate basket of stocks and send them to a specially designated custodial bank for safekeeping. These baskets are normally quite large, sufficient to purchase 10,000 to 50,000 shares of the ETF in question. The custodial bank doublechecks that the basket represents the requested ETF and forwards the ETF shares on to the authorized participant. This is a so-called in-kind trade of essentially equivalent items that does not trigger capital gains for investors.

The custodial bank holds the basket of stocks in the fund's account for the fund manager to monitor. There isn't too much activity in these accounts, but some cash comes into them for dividends and there are a variety of oversight tasks to perform. Some managers have leeway to use derivatives to track an index.

This flow of individual stocks and ETF certificates goes through the Depository Trust Clearing Corp., the same US government agency that records individual stock sales and keeps the official record of these transactions. It records ETF transfer of title just like any stock. It provides an extra layer of assurance against fraud.

Once the authorized participant obtains the ETF from the custodial bank, it is free to sell it into the open market. From then on ETF shares are sold and resold freely among investors on the open market.

Redemption is simply the reverse. An authorized participant buys a large block of ETFs on the open market and sends it to the custodial bank and in return receives back an equivalent basket of individual stocks which are then sold on the open market or typically returned to their loanees.

What motivates each player? The fund manager takes a small portion of the fund's annual assets as their fee, clearly stated in the prospectus available to all investors. The investors who loan stocks to make up a basket make a small interest fee for the favor. The custodial bank makes a small portion of assets likewise, usually paid for by the fund manager out of management fees. The authorized participant is primarily driven by profits from the difference in price between the basket of stocks and the ETF and on part of the bid-ask spread of the ETF itself. Whenever there is an opportunity to earn a little by buying one and selling the other, the authorized participant will jump in.

posted by writing staff @ 11:56 AM

0 comments

![]()

![]()

Even if you are new to investing, you may already know some of the most fundamental principles of sound investing. How did you learn them? Through ordinary, real-life experiences that have nothing to do with the stock market.

For example, have you ever noticed that street vendors often sell seemingly unrelated products - such as umbrellas and sunglasses? Initially, that may seem odd. After all, when would a person buy both items at the same time? Probably never - and that's the point. Street vendors know that when it's raining, it's easier to sell umbrellas but harder to sell sunglasses. And when it's sunny, the reverse is true. By selling both items- in other words, by diversifying the product line - the vendor can reduce the risk of losing money on any given day.

If that makes sense, you've got a great start on understanding asset allocation and diversification. This publication will cover those topics more fully and will also discuss the importance of rebalancing from time to time.

Let's begin by looking at asset allocation.

posted by writing staff @ 11:52 AM

0 comments

![]()

![]()

Buying Russian

posted by writing staff @ 11:33 AM

0 comments

![]()

![]()

A closed-end fund is a collective investment scheme with a limited number of shares.

In the U.S. legally they are called closed-end companies and form one of three SEC recognised types of investment company along with mutual funds and unit investment trusts. (Click here for US SEC description of investment company types).

Other examples of close-ended funds are Investment trusts in the UK and Listed investment companies in Australia.

New shares are rarely issued after the fund is launched; shares are not normally redeemable for cash or securities until the fund liquidates. Typically an investor can acquire shares in a closed-end fund by buying shares on a secondary market from a broker, market maker, or other investor -- as opposed to an open-end fund where all transactions eventually involve the fund company creating new shares on the fly (in exchange for either cash or securities) or redeeming shares (for cash or securities).

The price of a share in a closed-end fund is determined partially by the value of the investments in the fund, and partially by the premium (or discount) placed on it by the market. The total value of all the securities in the fund divided by the number of shares in the fund is called the net asset value, often abbreviated NAV. The market price of a fund share is often higher or lower than the NAV: when the fund's share price is higher than NAV it is said to be selling at a premium; when it is lower, at a discount to the NAV.

continue

posted by writing staff @ 11:28 AM

0 comments

![]()

![]()